Small margins make a big difference in business. For example, average credit card processing fees range between 1.5% and 3.5%. For utility companies, which handle a significant volume of transactions, these fees quickly add up, cutting into their already tight profit margins.

Many of these organizations are exploring alternative payment options, such as cash discount program integration for utility companies, to alleviate this financial burden.

Cash discount programs processing for credit unions and small banks can give these utility companies an option to incentivize cash payments from their customers. This reduces their dependence on costly credit card transactions.

How Do Cash Discount Programs Work?

Cash discount programs are designed to encourage customers to pay by cash or ACH instead of credit or debit cards.

The concept is fairly straightforward: a utility company offers a lower price or a discount to customers who pay their bills with cash and ACH instead of those who use credit or debit cards.

NOTE: Don’t confuse a cash discount and a surcharge. For a program to be called a cash discount, the posted price must be for cards, and then you offer a discount for customers who pay using cash.

So, to offer a cash discount, first, adjust the original price to cover the credit card processing fee.

For example, the listed price of the water bill would be adjusted to account for the credit card and ACH processing costs. Let’s assume the original water bill amount is $50.

The utility company would increase the listed price accordingly to recover the credit card processing fee or ACH transaction costs. Let’s say the credit card processing fee is 2.5%, and the ACH transaction cost is $1.50.

- Credit Card Payment: If a customer pays the water bill using a credit card, the listed price will be adjusted to $51.25 (original amount + 2.5% processing fee). The customer would then pay $51.25 using their credit card.

- ACH Payment: If the customer decides to pay through an ACH transaction, the listed price will be adjusted to $51.50 (original amount + $1.50 ACH transaction cost). The customer would pay $51.50 using the ACH payment method.

Cash payment - If the customer chooses to pay the water bill in cash, they would be eligible for the cash discount. In this case, the customer would pay $50, receiving a discount of $1.50.

Benefits of Cash Discount Programs for Small Banks and Credit Unions

Electronic cdp solutions for utility companies have effectively reduced transaction costs and driven customer behavior in the utility sector. But how exactly do they benefit banks and credit unions?

Fraud Prevention

According to a report by Federal Trade Commission, credit card fraud had the second most total losses. On the other hand, cash transactions inherently carry a lower risk of fraud compared to electronic payments.

By promoting cash payments through cash discount programs, small banks, and credit unions can minimize exposure to fraudulent activities, including:

- Payment card fraud

- Identity theft

- Unauthorized transactions

This protects the customers’ sensitive information, fostering trust and confidence in your services.

Operational Efficiency

Cash payments are typically simpler and faster to process compared to electronic transactions. Also, cash transactions often involve fewer intermediaries, reducing the complexity and potential delays associated with electronic payment systems.

This streamlined process saves time and allows staff to focus on other essential tasks.

Competitive Edge in the Market

In business, having a unique value proposition is a game changer. Cash discount programs are an opportunity to save money through cash payments. This is an attractive and tangible benefit that sets you apart from competitors.

The Advantages of Cash Discount Programs for Businesses

Cash discount programs offer numerous benefits to businesses, particularly those that process a high volume of transactions, such as utility companies.

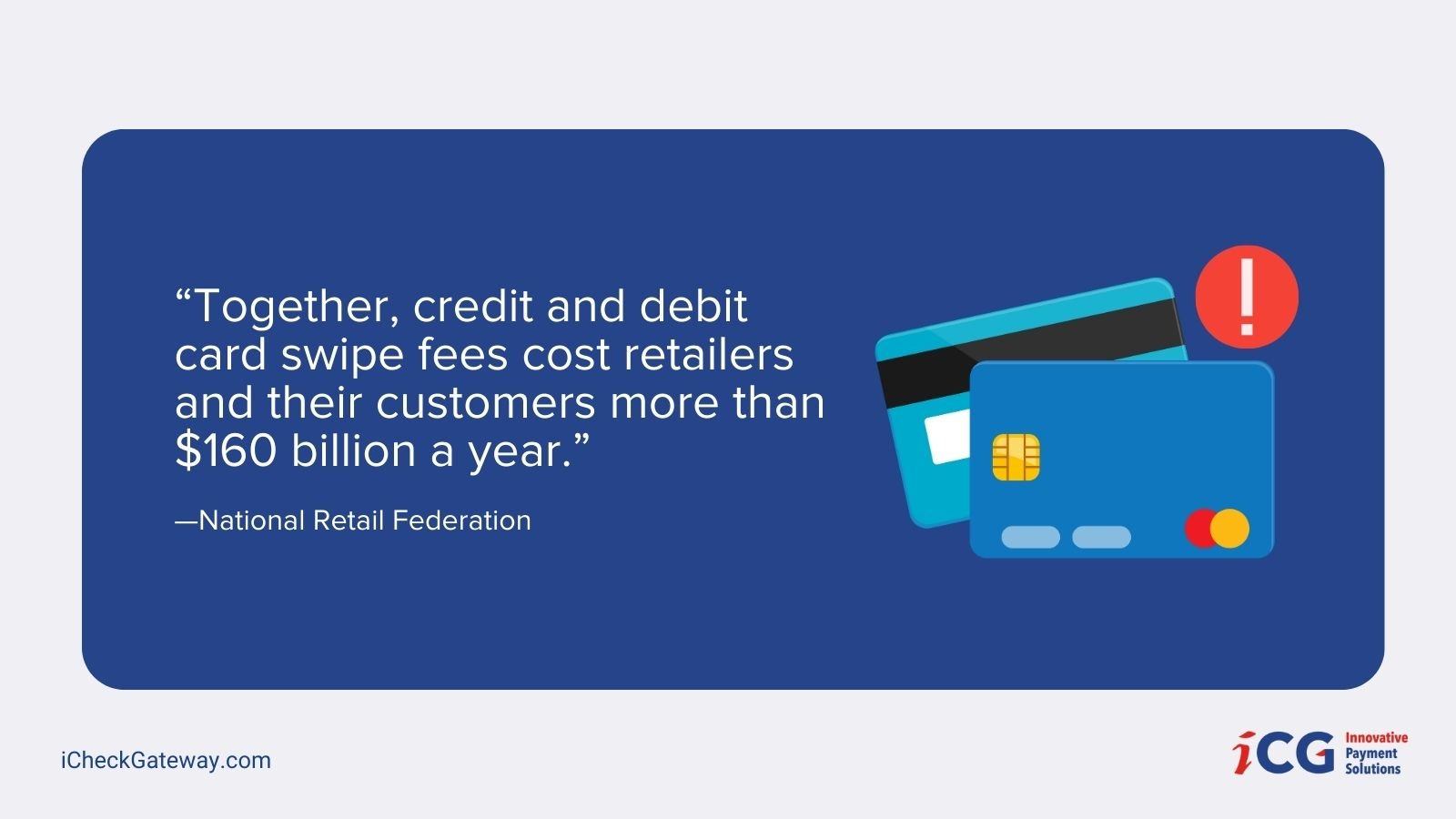

Cost Savings

“Together, credit and debit card swipe fees cost retailers and their customers more than $160 billion a year.”

—National Retail Federation

By encouraging customers to pay in cash, businesses significantly reduce these costs. For example, a utility company with annual credit card transactions of $1 million could save $15,000 to $35,000 annually, assuming a processing fee of 1.5% to 3.5%.

Improved Cash Flow

Cash flow is very important in business. With cash payments, funds are typically available immediately. The best utility company cash discount programs improve a business’s cash flow.

Businesses that receive more payments by cash have a lower Days Sales Outstanding (DSO) value, meaning they can collect their receivables more quickly.

Reduced Chargebacks

Many chargeback claims are legitimate, initiated by customers seeking refunds or disputing unauthorized transactions. However, businesses also face a risk known as friendly fraud, where some customers exploit a loophole to obtain unauthorized refunds while retaining the purchased goods or services.

A report by LexisNexis stated that in 2020, every dollar of fraud cost merchants $3.75. That means that for every dollar a U.S. merchant loses to fraud, they lose an additional $2.75. This is because of the fraud-related costs, such as chargebacks, customer support, and investigations.

But by reducing credit card transactions, businesses can also reduce the risk and cost of chargebacks.

The Advantages of Cash Discount Programs for Consumers

Save Money on Every Bill

Every dollar counts, especially when it comes to monthly expenses like utilities. You avoid the extra fees often associated with credit or debit card transactions by paying in cash. It’s as simple as that — pay in cash, save money.

No Risk of Identity Theft

Electronic payment methods require transmitting sensitive data, including card numbers, expiration dates, and security codes. Unfortunately, this information is vulnerable to interception or hacking attempts, potentially leading to identity theft and unauthorized access to your financial accounts.

However, by opting for cash payments, you eliminate the need to share any personal or financial information during the transaction.

Simple and Convenient

Paying in cash is straightforward and hassle-free. You won’t have to worry about remembering passwords, dealing with declined cards, or waiting for transactions to process. Plus, many utility providers are now offering easy in-person or secure drop-box payment options. It’s never been easier to pay your bills.

Easy Setup of Recurring Payments with ACH

Automated Clearing House (ACH) payments carry lower fees than card transactions. With ACH, you can set up automatic, recurring payments directly from your bank account. There is no need to remember due dates and no late fees, and you still enjoy the benefits of the cash discount program.

Implementing Cash Discount Programs

The first step is to conduct market research.

“42% of startups fail because they don’t meet a market need.”

—Newsday

So, before implementing a cash discount program, understand the needs of your commercial customers.

Conduct market research to identify utility companies’ main pain points regarding payment processing. Then design the secure cash discount payment processing for credit unions to address these issues effectively.

Next, partner with a payment processor. Why?

Payment processors specialize in handling payment transactions and have extensive knowledge and experience in the industry. Instead of developing infrastructure and systems to handle everything yourself, a strategic collaboration with a payment processor allows you to leverage their specialized expertise.

Finally, there are legal and regulatory frameworks that govern the use of cash discount programs, ensuring fair and transparent practices for businesses and consumers alike. Let’s look at some of them:

Legal and Regulatory Requirements of Cash Discount Programs

Cash discount programs are legal in most jurisdictions, but it’s critical to ensure that they are implemented in compliance with all relevant laws and regulations:

- Truth in Lending Act (TILA) - This federal law requires that customers are fully informed about the terms and conditions of their financial transactions. As such, businesses must clearly communicate that a service fee applies to card transactions and that this fee can be avoided by paying in cash.

- Card Network Rules - Major card networks like Visa and Mastercard have rules about how cash discount programs should be operated. Typically, these rules require that the cash discount is offered to all customers and applies to all forms of payment, not just cards.

- State Laws - Some states have surcharges and cash discounts laws, so it’s important to check the laws in each jurisdiction where the program will be offered.

Promoting Cash Discount Programs

Now it’s time to get the word out there. How do you effectively do it?

- Highlight the benefits - Ensure your marketing materials clearly communicate the program’s benefits. For businesses, emphasize cost savings, improved cash flow, and reduced fraud risk. For consumers, focus on savings, transparency, and convenience.

- Use multiple channels - Utilize a mix of marketing channels to reach your audience, including direct mail, email, social media, and in-branch promotions.

- Educational workshops and webinars - Consider hosting workshops or webinars to educate businesses and consumers about the benefits of cash discount programs and how they differ from surcharges.

Summary

Cash discount programs technology for banks offer a win-win situation for small banks, credit unions, and consumers.

But how do you make the transition and implement a cash discount program?

Partner with us at iCheckGateway.com. We help you incentivize cash and ACH bank transfer payments to ensure you don’t lose money from credit card processing fees. We also help you set up cash discount programs for your bank and credit union as per your region’s legal and regulatory framework. Schedule a discovery call with us to learn more.